Accenture's AI-Driven Growth Sets the Stage for Indian IT's Mixed Q1FY26 Outlook: What to Expect from Upcoming Results Season?

How Accenture's GenAI bookings and strategic reinvention offer a roadmap for Indian IT companies navigating demand uncertainty and the promise of mid-cap outperformance in Q1FY26.

Accenture Q3 FY25: Navigating Uncertainty with Strategic Reinvention

The consulting giant's latest quarterly results reveal that the company has adapted to an increasingly complex business environment. While the headline numbers are solid: $17.7 billion in revenue, up 7% in local currency, and earnings per share growth of 12%; the real story lies in how Accenture is positioning itself for the future amid what CEO Julie Sweet describes as "significantly elevated uncertainty."

The Reinvention Imperative

What stands out most clearly from Accenture's Q3 performance is the fundamental shift in client behavior. Companies are no longer making incremental technology investments or pursuing discretionary projects. Instead, they're committing to large-scale, foundational transformations that will define their competitive position for years to come.

This shift is evident in the numbers: 30 clients signed deals worth over $100 million each in the quarter, reflecting a clear preference for comprehensive reinvention over piecemeal solutions. Since April 2022, when Accenture first articulated its strategy to become the "reinvention partner of choice," the company has secured nearly 400 such large-scale engagements.

The nature of these deals has evolved significantly. Rather than the traditional approach of implementing technology first and adding intelligence later, clients are now demanding AI-native solutions from the outset. This represents a maturation of the market's understanding of what digital transformation actually requires in the age of artificial intelligence.

Generative AI: Beyond the Hype

Accenture's generative AI business continues to demonstrate remarkable momentum, with $1.5 billion in bookings for the quarter and over $700 million in revenue, bringing year-to-date totals to $4.1 billion in bookings and $1.8 billion in revenue. However, the company's approach to AI reveals a more nuanced understanding of the technology's true value proposition.

The examples Accenture shared illustrate this sophistication. For Pfizer, the company is deploying "Agentic AI" that can proactively monitor and resolve IT issues without human intervention. For Nestlé, AI-powered digital twins are reducing content creation time and costs by over 70%.

CEO’s commentary on this point is particularly insightful: "Gen AI alone is just a tool. The work needed to use Gen AI to create value at scale is substantial".

Although, Accenture is claiming that they are embedding GenAI in all of their business deals and GenAI is turning out to be revolutionary for the companies, I feel that the use case of AI is still very much limited from the examples shared by the company.

For example, let’s take a look at the work they are doing for Air France-KLM. A simple cloud migration has been tagged with AI with no definite outline of how AI is of help here. Specifically, what has AI enabled here in cloud migration that was not possible before?

Similarly, for Pfizer, the application doesn’t seem more than a simple chatbot with "intelligent” features. I would love to know in the comment section if any of the reader can point out otherwise.

As a final example, for Tronox, we can see a lot of buzz-words were used around GenAI like ‘productivity’, ‘efficiency’. However, I lack to see genuine use cases where AI is pushing the boundary.

Reorganization and Financial Discipline

Accenture has take a decision to consolidate its Strategy, Consulting, Song, Technology, and Operations units into a single business called "Reinvention Services," effective September 11. This is a strategic restructuring designed to accelerate solution delivery and embed AI more deeply across all offerings.

This represents the third major organizational transformation in Accenture's recent history. The company restructured in 2013 to capitalize on the digital transformation wave, achieving a 9% compound annual growth rate through 2019. It reorganized again in 2020 to scale those digital capabilities globally, delivering a 10% CAGR from 2020 to 2025. Each transformation has coincided with a major technology inflection point, and each has driven significant growth.

Operationally, Accenture continues to demonstrate strong financial discipline. The company expanded its operating margin to 16.8%, up 40 basis points from the adjusted prior-year quarter, while simultaneously investing heavily in talent development and strategic acquisitions. Free cash flow reached $3.5 billion, and the company returned $2.7 billion to shareholders through dividends and buybacks.

The slight decline in new bookings, down 7% in local currency deserves attention, though management attributes this to market conditions rather than competitive pressures. The quality of bookings remains high, with a book-to-bill ratio of 1.1 and a strong pipeline heading into Q4.

Notably, the pace of acquisitions has slowed this year, with $789 million invested across 15 deals compared to more aggressive acquisition activity in previous years. Management frames this as disciplined capital allocation rather than a strategic shift, emphasizing that they won't pursue acquisitions that don't meet their economic criteria.

Looking Forward

Accenture has raised its full-year revenue guidance to 6-7% growth in local currency, with operating margin expected at 15.6% and diluted earnings per share in the range of $12.77-$12.89. The company expects to return at least $8.3 billion to shareholders through dividends and buybacks.

The real test will be whether the new organizational structure can deliver on its promise of accelerated growth. History suggests that Accenture has a strong track record of successfully navigating major transitions, but the current environment presents unique challenges. The convergence of economic uncertainty, geopolitical complexity, and rapid technological change creates a more complex operating environment than the company has previously faced.

What's clear is that Accenture has positioned itself at the center of the most important business transformation of our time. As companies grapple with the implications of artificial intelligence, they need partners who understand not just the technology, but how to integrate it into the fabric of their operations. Accenture's Q3 results suggest it's well-positioned to capitalize on this opportunity, but the ultimate measure of success will be its ability to sustain growth as the market continues to evolve.

Indian IT Sector Q1FY26 Results Preview: Navigating Through Uncertainty

As we approach the Q1FY26 earnings season for Indian IT companies, which kicks off with TCS and Tata Elxsi on July 10th, the sector finds itself at an interesting crossroads. The landscape ahead appears challenging yet nuanced, with cross-currency tailwinds providing some relief while underlying demand conditions remain subdued.

The Cross-Currency Silver Lining

One of the most significant factors supporting the sector this quarter will be favorable cross-currency movements. The depreciation of the USD against major currencies like EUR, GBP, AUD, CAD, and JPY is expected to provide a substantial tailwind of 100-300 basis points across companies. This means that while organic constant currency growth may appear muted, reported USD revenue growth will look considerably more robust.

For instance, companies with higher European exposure are likely to benefit more significantly from these currency movements. The EUR has strengthened by approximately 8.6% against the USD quarter-on-quarter, while GBP has gained 6.4%. This currency support will be particularly visible for companies like TCS and Infosys, which have diversified geographic revenue streams.

A Tale of Two Tiers

The earnings season is shaping up to reveal a stark contrast between large-cap and mid-cap IT companies. Among the tier-1 players, street is expecting largely muted performance with sequential constant currency revenue growth ranging between -2.8% to +1.5%. Only Infosys and LTIMindtree are expected to post positive q-o-q growth in constant currency terms, with most others likely to report revenue declines.

Wipro appears positioned for the weakest performance among large-caps, with expectations of a -2.8% decline in constant currency terms. This reflects the company's ongoing struggles with demand weakness and project ramp-downs. Meanwhile, TCS faces headwinds from the tapering of its BSNL deal, which has been a significant revenue contributor in recent quarters.

The mid-cap story, however, presents a more encouraging narrative. Companies like Coforge and Persistent Systems are expected to deliver strong growth, with Coforge’s street expectation being 5.8% q-o-q growth in constant currency terms, driven by the ramp-up of its landmark Sabre deal. Persistent Systems is also expected to maintain its momentum with around 4.5% growth, primarily led by strength in BFSI and healthcare verticals.

The Demand Environment Reality Check

The underlying demand environment continues to reflect the cautious stance that enterprises have adopted in response to ongoing macroeconomic uncertainty. The 90-day pause in US-China tariff tensions has provided some respite, but it hasn't translated into a meaningful uptick in new deal closures. Clients remain in a "wait-and-watch" mode, carefully evaluating the impact of potential policy changes on their cost structures and supply chains.

This cautious approach is particularly evident in discretionary spending, which remains subdued across most verticals except BFSI. Manufacturing, retail, and automotive sectors continue to face headwinds, while the communication vertical shows mixed signals. The silver lining lies in the fact that demand deterioration has been lower than initially anticipated at the start of the quarter, allowing companies to maintain their full-year guidance.

Margin Dynamics in Focus

Margin performance this quarter will largely depend on companies' ability to manage the competing forces of currency tailwinds and operational challenges. Most tier-1 companies are expected to report margins within a narrow range, with movements of -80 to +50 basis points q-o-q.

Tech Mahindra and LTIMindtree stand out as potential margin expansion stories, with both companies expected to benefit from their ongoing operational improvement initiatives. Tech Mahindra's Project Fortius continues to focus on high-margin segments, while LTIMindtree's cost control measures are expected to drive a 50 basis point improvement. (More about Tech Mahindra’s Project Fortius here: Link)

However, companies like HCL Technologies may face margin pressure due to revenue decline and the absence of operating leverage. The company's margin is expected to decline by around 80 basis points, reflecting the challenges of maintaining profitability in a low-growth environment.

The GenAI Momentum Continues

One of the more positive themes emerging from the sector is the continued momentum in Generative AI initiatives. While still in relatively early stages, companies are moving beyond proof-of-concept implementations to full-scale deployments. This transition represents a meaningful shift in how enterprises are approaching AI adoption, moving from experimental phases to production-ready solutions.

The AI opportunity is becoming increasingly embedded across service offerings, with companies reporting growing revenue contributions from AI-related projects. However, the real value creation is happening through the integration of AI with existing business processes, data architectures, and industry-specific solutions rather than standalone AI implementations.

Deal Pipeline and Client Spending Patterns

The deal pipeline across the sector remains robust, though the nature of deals is evolving. There's a clear shift toward cost optimization and vendor consolidation deals, reflecting clients' focus on efficiency rather than growth-oriented digital transformation projects. Large deal closures are expected to be limited this quarter, but the overall pipeline suggests a solid foundation for future growth.

TCS is expected to report deal bookings in its usual range of USD 7-9 billion, while Infosys may see bookings around USD 2.5 billion. For mid-cap companies, the deal momentum varies, with some like Mphasis expecting strong total contract values of USD 400-450 million.

Sector Outlook and Investment Implications

Looking ahead, the sector's near-term prospects remain cautiously optimistic. While Q1FY26 is likely to be another soft quarter, there are signs that the worst of the demand downturn may be behind us. The expectation is for a back-ended recovery in the second half of FY26, contingent on macroeconomic stability and faster deal ramp-ups.

The divergence in performance between large-cap and mid-cap companies is likely to continue, with mid-caps potentially offering better growth prospects due to their agility and ability to capture market share. However, this comes with higher execution risk and greater sensitivity to market volatility.

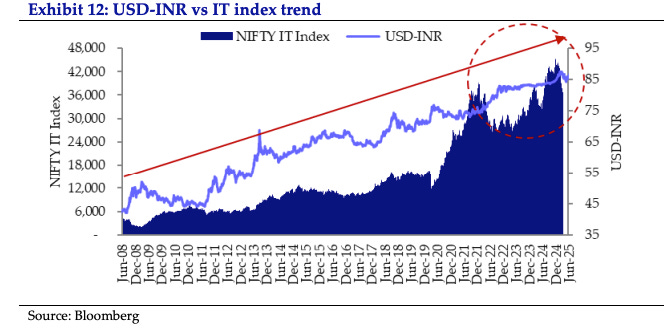

From a valuation perspective, the sector appears reasonably positioned. The IT index trades at around 25x forward earnings, which is approximately 2% below the five-year average but 19% above the ten-year average. This suggests that while valuations aren't cheap, they're not at extreme levels either.

As we head into the earnings season, investors will be closely watching management commentary on demand trends, deal conversion rates, and guidance for the remainder of FY26. The sector's ability to navigate the current uncertainty while positioning for the anticipated recovery will be crucial in determining its performance trajectory over the coming quarters.

| A guest post by

|