Has the Time for Tech Mahindra come? Q2FY25 Earnings Analysis

With Project Fortius underway, there are some early signs of green shoots visible. Should the company be in your radar? Let's take a look👇

Tech Mahindra (NSE: TECHM) reported its Q2FY25 results on 19th October and we can see some early signs of positivity thanks to Project Fortius and the efforts by upper management. Tech Mahindra reported strong financial results for Q2FY25, with consolidated net profit surging 153% year-on-year to Rs. 1,250 crores and revenue growing 3.5% year-on-year to Rs. 13,313 crores. The company's performance exceeded market expectations, with net profit significantly beating analyst estimates of around Rs. 900-950 crores, while revenue came in largely in line with forecasts of Rs. 13,200-13,400 crores. The robust profit growth was driven by improved operational efficiency, cost optimization measures, and a favorable business mix.

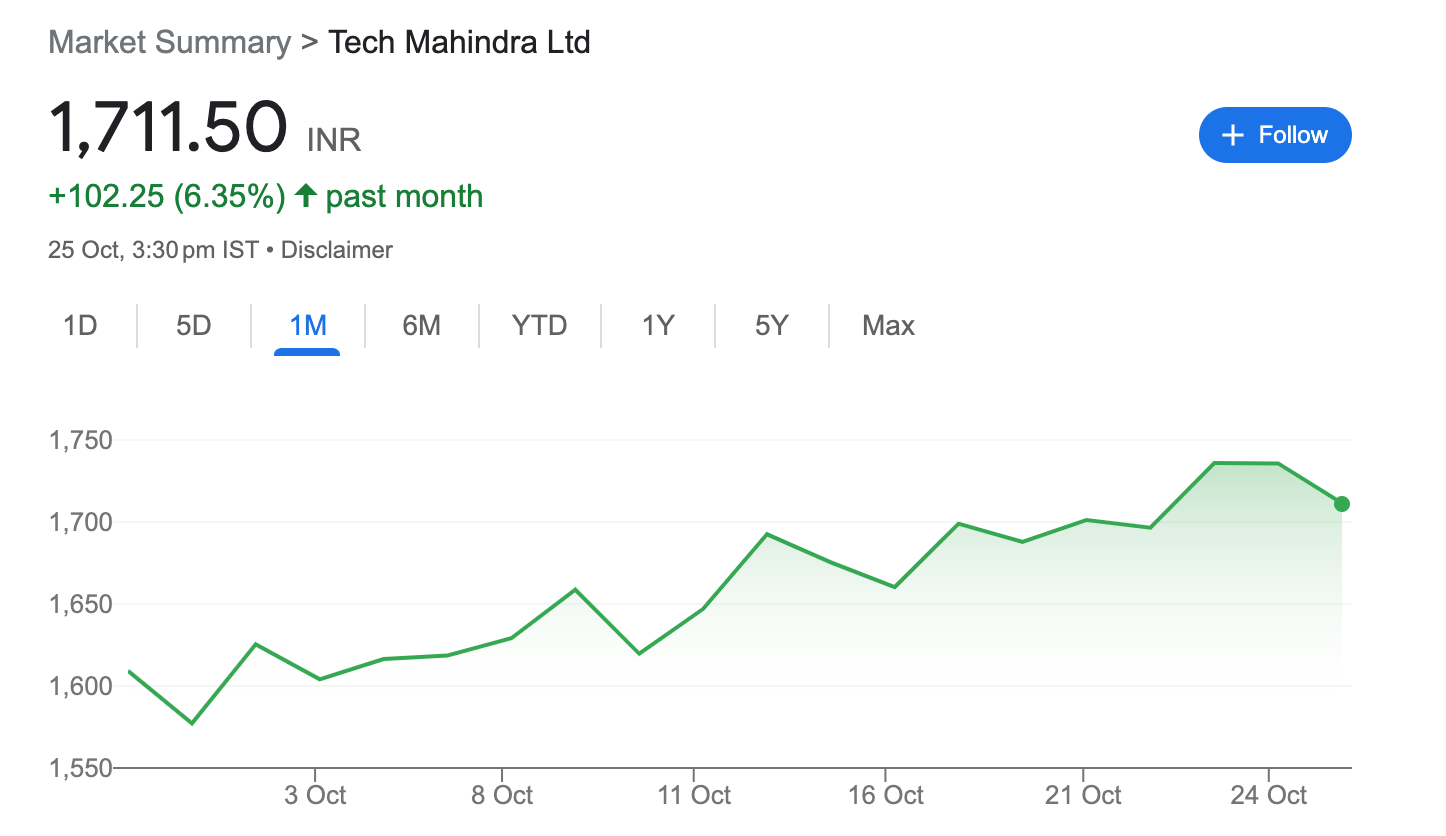

The stock price showed some positivity around results announcement, however, the enthusiasm has tapered off a bit, owing to the selloff in the Indian Markets lately.

Financial Analysis:

In the second quarter of FY25, Tech Mahindra reported a total revenue of USD 1,589 million, reflecting a steady YoY growth of 2.2% and a QoQ increase of 1.9%. On a constant currency basis, revenue grew by 0.7% QoQ and 1.2% YoY. This growth translated to ₹13,313 crores in Indian Rupee terms, representing a 2.4% rise QoQ and 3.5% YoY.

The company posted a notable improvement in its profitability metrics, driven by margin expansion initiatives under “Project Fortius.” The EBIT margin for Q2FY25 stood at 9.6%, an increase of 110 basis points from the previous quarter, aided by both operating efficiencies and favorable currency movements. This margin expansion was mainly attributed to Project Fortius, which contributed about 70 basis points to overall improvements. PAT margins also saw a significant jump, closing at 9.4%, up by 280 basis points QoQ, with the profit after tax reported at USD 149 million, or ₹1,250 crores.

In terms of cash generation, Tech Mahindra reported free cash flow (FCF) of USD 157 million, which translates to a robust 105.4% of its PAT, underscoring the company’s efficient cash management and strong operating cash generation capabilities. The company ended the quarter with cash and cash equivalents of USD 784 million (₹6,566 crores). Reflecting its positive cash position and commitment to shareholder returns, Tech Mahindra declared an interim dividend of ₹15 per share for Q2FY25.

Operationally, Tech Mahindra made strides with its workforce and productivity initiatives. The company added 6,653 employees during the quarter, bringing the total headcount to 154,273. Utilization rates, including trainees, rose slightly to 86.3%, showcasing enhanced efficiency. Additionally, the company achieved a notable improvement in its attrition rates, with last-twelve-months (LTM) attrition declining by 80 basis points year-over-year to 10.6%. For a company of this size, both the attrition and utilization rate are best in class.

Segment and Geographical Analysis:

Segment Analysis

Tech Mahindra’s segment performance for Q2FY25 highlights a mix of steady growth and some pressure in specific sectors. The Communications segment, which remains the largest contributor with a 33.4% revenue share, faced a 1.7% decline year-over-year, reflecting some softness in spending from telecom clients. However, it saw a 2.7% QoQ growth, hinting at potential stabilization. Manufacturing, which contributes 17.2% to total revenue, had a modest 0.6% YoY growth but experienced a 4% decline QoQ, largely due to ongoing softness in discretionary spending in this sector.

The Banking, Financial Services, and Insurance (BFSI) segment, comprising 15.8% of total revenue, performed well, recording a strong 4.5% YoY increase and a 2.4% QoQ rise. The company’s emphasis on expanding within BFSI, especially in areas like asset management and insurance, appears to be yielding positive results. Other sectors, such as Technology, Media, and Entertainment (TME) and Retail, Transport & Logistics, also demonstrated healthy growth with YoY increases of 2.4% and 4.7%, respectively. Notably, the Healthcare & Lifesciences segment grew 4.5% YoY, although it saw a slight decline of 1.8% QoQ, while the Others segment, a smaller but rapidly growing area, posted an impressive 29.5% YoY and 7.8% QoQ growth.

Geographical Analysis:

Regionally, Tech Mahindra’s performance reflected both strengths and some headwinds. In the Americas, revenue declined by 2% YoY and 0.7% QoQ. This softness is primarily attributed to weaker demand, particularly in the telecom and communications sectors. Europe, on the other hand, emerged as a strong region, delivering a 4.1% YoY growth and a 4.6% QoQ increase. This growth was underpinned by new client wins and a strong pipeline in key verticals. Rest of the World (ROW) recorded the highest growth rates, with a 9.7% YoY and 5% QoQ increase, signaling positive momentum in the Asia-Pacific and Middle Eastern markets, where Tech Mahindra has made strategic inroads.

Tech Mahindra and Telecom Clients - Big Potential Beneficiaries of Upcoming Rate Cuts?

The company has a significant exposure to telecom sector with majority chunk of their Top-5 clients being from the telecom sector. Tech Mahindra observed continued challenges in the telecom sector as clients focused on cost-saving measures, resulting in reduced discretionary spending. This shift led to a 1.7% year-over-year decline in the communications vertical, the company’s largest revenue contributor at 33.4%. Nonetheless, the sector showed some sequential improvement with 2.7% growth quarter-over-quarter, marking its first positive growth in five quarters.

The debt burden in the telecom industry, compounded by rising interest rates, has placed additional pressure on these clients, further constraining their budgets. Many telecom companies have become more cautious, scaling back on larger projects and prioritizing essential, cost-efficient operations. To address these needs, Tech Mahindra has focused on supporting telecom clients in achieving operational efficiencies and enhancing customer experience through autonomous operations programs. Leveraging its capabilities in network services, AI, and workforce transformation, Tech Mahindra is helping clients navigate these financial constraints.

Despite the sector’s challenges, Tech Mahindra continues to secure partnerships in Europe and Australia, where it will lead digital transformation and customer experience initiatives for telecom operators. These efforts reflect the company’s adaptive strategy to maintain long-term relationships in a sector facing significant financial headwinds. Moreover, with the upcoming rate cuts by the Federal Reserve, the company is hopeful that discretionary spending will make a comeback for Telecom Sector.

BFSI To Provide Earnings Boost?

Tech Mahindra’s management highlighted the financial services sector as a significant growth opportunity, given its position as the largest global spender on IT services. Currently contributing 15.8% of Tech Mahindra’s revenue, the company aims to increase its presence in this under-indexed vertical. This strategic focus is being executed through a multi-pronged approach:

1. Leadership Augmentation: New leadership has been introduced across regions to deepen expertise in financial services, including professionals from major firms such as Infosys, HCL, and Accenture.

2. Differentiated Capabilities: Tech Mahindra has established unique strengths in areas like core banking, asset and wealth management, and insurance, including specialized capabilities in Guidewire and digital engineering.

3. Cross-Selling Strategy: With a strong existing client base, the company aims to expand engagements, targeting some accounts for potential growth to USD 100 million in annual business.

Additionally, management leveraged the CEO’s relationships to secure two major empanelments, including one with a leading U.S. cards and payments provider for a modernization program and another with a European bank for a core banking transformation. The management also confirmed that they are seeing some elevated earnings spend in BFSI vertical and hinted that discretionary spending might be making a comeback. However, they would want to wait for couple of more quarter before declaring it as a trend.

Other Highlights:

Here’s a summary of the management commentary on Tech Mahindra’s Q2FY25 performance across key areas:

Total Contract Value (TCV) and Margin Improvements:

TCV Performance: Tech Mahindra achieved total TCV of USD 603 million for Q2FY25, marking an improvement over the six-quarter average. This increase was attributed to strategic deal wins across telecom, media, and financial services.

Margin Discipline: The company is focused on profitable deals and has avoided those requiring “heroic productivity assumptions” that could compress margins. Efforts to improve margins were supported by operating efficiencies, strict contract governance, and increased offshore work, driving a sequential EBIT margin increase of 110 basis points.

Weakness in Manufacturing and Auto Sector:

Manufacturing: This segment saw YoY growth of just 0.6% but declined by 4% quarter-over-quarter, highlighting demand softness.

Auto Sector Challenges: Margin compression across auto clients impacted growth, with several clients showing weakened profitability in Q2FY25. The company indicated that elevated interest rates and a challenging macroeconomic environment continue to weigh on both manufacturing and auto verticals.

Large Deal Commentary (with Margin Focus):

Large Deal Strategy: Company has invested heavily in strengthening its large-deal capabilities by hiring deal architects, technical architects, and skilled negotiators. Although large deals remain critical for growth, management underscored that profitability is prioritized over volume, maintaining a disciplined approach to avoid deals that may strain future margins.

Caution on Assumptions: The company remains cautious about multi-year deals with aggressive productivity assumptions, instead focusing on deals that align with its margin targets and technological capabilities.

FY26 Guidance:

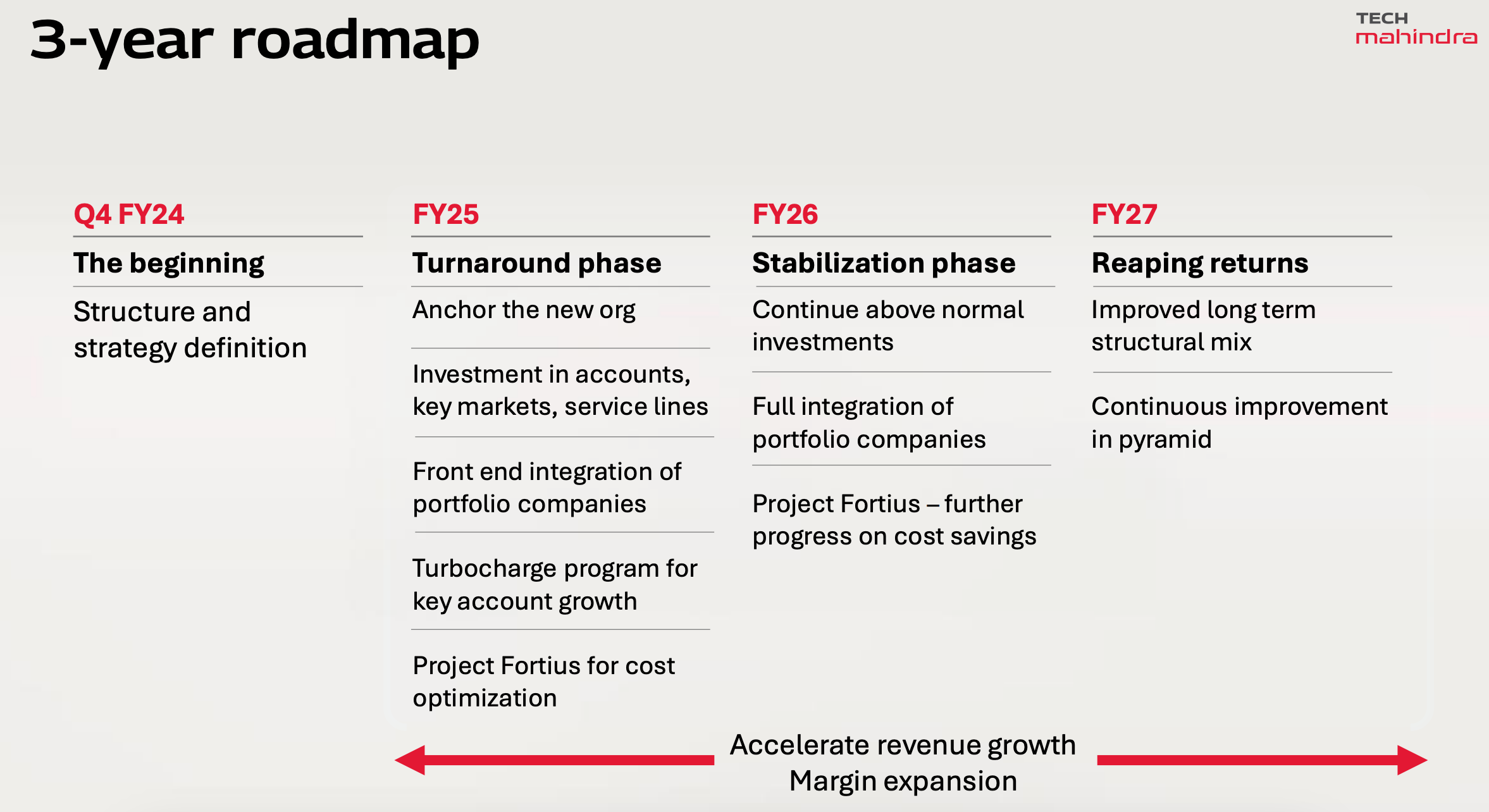

Strategic Focus: FY26 is considered a stabilization phase in Tech Mahindra’s turnaround journey, with continued investments, though at a reduced rate compared to FY25. Management expects to reap the benefits of its efficiency and integration initiatives, which are anticipated to support stronger revenue growth and margin expansion by FY27.

Long-Term Margin Target: Tech Mahindra aspires to reach an EBIT margin of 15% by FY27, supported by Project Fortius, which aims for annual cost savings of USD 250 million. The company has also committed to returning at least 85% of free cash flow to shareholders over the next five years.

Management on AI and BPO Deal Wins:

Tech Mahindra’s management highlighted that AI is not expected to reduce revenues from their Business Process Outsourcing (BPO) segment. Mohit Joshi, CEO, noted that while GenAI could disrupt traditional contact center roles, Tech Mahindra is actively adapting its BPO portfolio to higher-value services. These services include analytics, vertical-specific solutions, and crowd-sourcing platforms, which align with emerging AI trends. The company also focuses on building AI-enabled contact centers, differentiating itself from other pure-play BPO providers by embedding AI expertise across operations.

Further, management expressed confidence in long-term growth prospects for BPO, emphasizing the role of AI in enhancing, rather than replacing, business opportunities. They highlighted demand in sectors like high-tech, financial services, and healthcare, where the company sees expanded opportunities with AI integration.

What is Project Fortius and How is it going to impact the company?

Project Fortius is a key initiative by Tech Mahindra aimed at structural improvements to drive long-term cost efficiencies and enhance profitability. The project is central to Tech Mahindra’s transformation strategy and aims for annual cost savings averaging USD 250 million over the FY25–FY27 period. It focuses on several critical areas, including operational efficiency, organizational restructuring, and optimized contract governance. This project is projected to make a significant contribution to margin improvement, helping Tech Mahindra target an EBIT margin of 15% by FY27.

Margin Expansion: Project Fortius has already contributed to sequential EBIT margin expansion, with Q2FY25 margins increasing by 110 basis points. The project’s efficiencies come from a combination of contract optimization, reducing subcontractor dependencies, and expanding offshore work, all of which improve profitability on existing deals. FY26 would be the stabilization phase, during which investments will continue but at a slower rate. By FY27, Tech Mahindra expects to fully benefit from the savings and efficiencies achieved, leading to accelerated revenue growth and expanded margins.

Revenue Synergies and Cost Synergies: Fortius promotes integration across Tech Mahindra’s acquired portfolio companies, focusing on synergies that enhance both revenue and operational efficiency. This integration will support Tech Mahindra’s efforts to grow key client accounts and focus on high-yield markets.

Am I buying the stock at current levels?

While the Q2FY25 earnings has beaten the street estimates and the management is walking the talk with Project Fortius underway, the stock is trading at 24x September 26 EPS. With the revamp planned, I feel that there is definitely upside to the company that we will be witnessing in the upcoming quarters. But, with the current stock price and the heavy sell offs in the Indian markets, I would wait a bit before initiating a position in the company. Either, I would wait for the stock price to decline 5-10% or track the following factors to forecast how the company might fare up in the coming quarters:

Rate Cuts by the Federal Reserve and comeback of discretionary spending in telecom sector - Especially when the Top-5 clients and 33.4% of the revenue is dependent on this sector alone.

Discretionary spending in BFSI - especially in Investment Management, cards and payment providers where the management’s focus has been.

Project Fortius updates - Attrition rate especially amongst senior leadership, hiring of the freshers and margin expansion roadmap.