TCS Q3FY25 Results: Deal Momentum picks up hinting at bottoming out of Discretionary Spend Slump

The results were described as "modest," but positive management commentary led to a 5% jump in TCS shares following the announcement

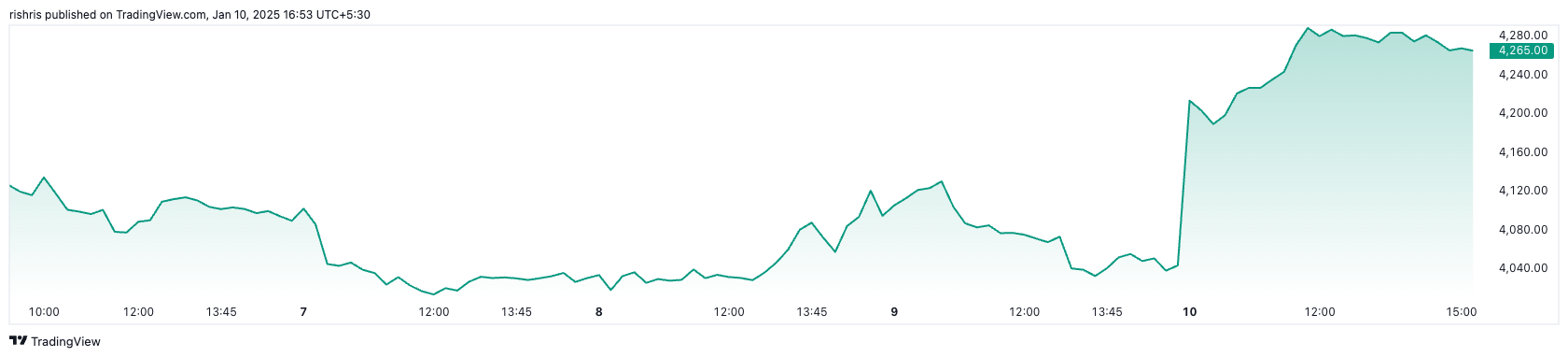

TCS announced their Q3FY25 results yesterday with consolidated revenue of ₹63,973 crore, reflecting a 5.6% year-on-year (YoY) growth from ₹60,583 crore in Q3 FY24. The operating margin stood at 24.5% which is a sequential improvement of 40bps, but a y-o-y decline of 50bps. The market reacted positively to the results with TCS’ stock soaring 5.6% today:

Financial Analysis:

Revenue Performance:

Revenue growth was flat sequentially in C.C. terms, with a modest 4.5% YoY increase.

In USD terms, revenue declined 1.7% QoQ, slightly below expectations.

Profitability and Margins:

EBIT margin improved by 40 bps QoQ to 24.5%, driven by operational efficiencies like increased productivity, better resource utilization, and pyramid rationalization.

The margin exceeded some estimates by 10 bps, and management is targeting a 26% margin by FY25-end.

Net profit rose by 3.4% YoY, aligning with forecasts.

Sectoral and Geographical Analysis:

TCS’s performance in Q3FY25 was a mixed bag, with some sectors and geographies showing resilience while others faced challenges.

Sectoral:

In the BFSI sector, there was marginal growth of 0.9% YoY in C.C. terms. Management highlighted positive factors like easing inflation, falling unemployment, and stable governance, but noted that geopolitical issues continue to weigh on the sector. Clients remain focused on improving operational efficiency and modernizing IT infrastructure, with BFSI leading the adoption of AI and GenAI.

The consumer business grew by 1.1% YoY in CC terms, with management signaling early signs of recovery in the retail segment, suggesting it may have bottomed out. Manufacturing reported modest growth of 0.4% YoY in CC terms, though macroeconomic challenges in the auto and aerospace sectors weighed on performance. Management expects the sector to stabilize in Q4 and rebound thereafter, supported by investments in smart manufacturing, software-defined vehicles (SDVs), and GenAI. Life Sciences & Healthcare, however, saw a decline of 4.3% YoY, impacted by policy uncertainty in the US and a one-off client issue in Q2. Despite these challenges, the sector is showing signs of stabilization.

Other verticals faced significant headwinds. Communication & Media declined sharply by 10.6% YoY in CC terms, while Technology & Services saw a marginal decline of 0.4%. On the other hand, Energy, Resources & Utilities achieved steady growth of 3.4% YoY. The standout performer was the Regional Markets & Others segment, which posted a remarkable 40.9% YoY growth in CC terms, leading all verticals.

Geographical:

Geographically, India was a bright spot, delivering exceptional growth of 70.2% YoY in CC terms, driven primarily by the non-BSNL business. Management plans to offset revenue from the BSNL deal with other projects in the region. Latin America and the Middle East & Africa also performed well, with YoY growth of 7.0% and QoQ growth of 7.7%, respectively.

However, North America saw a 2.3% YoY decline in CC terms, with a 1.5% QoQ drop, despite BFSI growth in large accounts. The UK grew by 4.1% YoY but experienced a 4.0% QoQ decline, while Continental Europe struggled with a 1.5% YoY and 6.4% QoQ decline. Asia Pacific also faced challenges, with revenue declining 4.2% QoQ.

BSNL Deal to Ramp-Down soon - Will it impact the Revenue?

The management commented that the BSNL deal is 70% complete and would be in ramp down mode very soon. The ramp-down of the BSNL deal is set to significantly impact TCS’s revenue growth in FY26, as the deal transitions from being a key contributor in FY25 to a headwind. While the BSNL project added 3.2% to FY25E revenue growth, it is expected to reduce FY26E growth by 3.6%, leading to an optically weak overall growth rate of 2.9%. However, excluding the BSNL impact, TCS’s core growth is estimated at 6.5%. Despite this challenge, TCS is exploring new opportunities in India and globally to replace the revenue gap, leveraging its BSNL capabilities and a robust deal pipeline to drive future growth.

On the positive side, the BSNL ramp-down is expected to improve TCS’s EBIT margins, which were impacted by 100 bps in FY25E due to increased third-party costs. As these costs decline and the product mix improves, margins are likely to normalize in FY26. Management remains confident that new deals and strategic investments will help mitigate the revenue loss while strengthening profitability. Though the BSNL deal’s wind-down will present short-term revenue challenges, it positions TCS for stronger margins and sustainable growth in the long term.

Demand driver - why does the management think CY25 will be better than CY24?

TCS management expects CY25 to perform better than CY24 due to several encouraging factors. They have observed early signs of a revival in discretionary spending, with clients increasingly prioritizing investments in cloud services, AI, and GenAI. Additionally, easing macroeconomic pressures such as lower inflation, reduced interest rates, and greater stability in U.S. governance are expected to bolster IT budgets and discretionary demand.

The strong pipeline of deal wins, particularly in BFSI and retail, further contributes to their optimism. Management also highlighted shorter deal cycles and increased activity in areas like application modernization, data projects, and AI-driven initiatives. These trends, combined with strategic investments and a focus on leveraging AI for business transformation, provide confidence that CY25 will witness stronger growth momentum despite headwinds such as the BSNL ramp-down.

Agentic AI - New talk of the Town?

TCS highlighted the growing importance of Agentic AI as the next level of maturity in AI adoption. Unlike earlier AI deployments focused on tasks like chatbots, Agentic AI enables businesses to orchestrate transactions and processes across their value chains by leveraging the advanced planning and reasoning capabilities of large language models (LLMs). TCS emphasized how its deep contextual understanding of client businesses allows it to design, train, and deploy AI agents that address high-value business problems effectively.

Examples of TCS Using AI for Customers

Customer Engagement for a U.S. Electronics Retailer

TCS implemented a unified contact center platform using advanced natural language understanding and conversational agents.

The system supports over 30,000 daily chat conversations and significantly improved key metrics, including a 3% increase in user containment and a 90% intent identification accuracy.

Cancer Drug Discovery for a Life Sciences Company

TCS used a GenAI-based drug discovery solution to design novel molecules for a cancer target protein with no existing dataset.

Around 1,300 molecules were generated and optimized, with 12 shortlisted for in-vitro assessments.

Fraud Detection for a Global Bank

TCS developed an AI-led real-time fraud detection solution that monitors transactions, identifies customer behavior anomalies, and generates risk scores.

The solution achieved an 18% improvement in fraud detection and reduced false positives by 25%.

Retail Expansion for a U.S. Luxury Fashion Retailer

TCS deployed a scalable omnichannel system to adapt to European markets, enabling faster market entry with local language and payment integrations.

The system reduced onboarding cycle time by 30% and streamlined operations, fostering customer loyalty and driving sales.

Hiring and Attrition Analysis:

TCS Hiring and Attrition Summary for Q3FY25

TCS reported a net headcount reduction of 5,370 employees in Q3FY25, bringing the total workforce to 607,354. Management attributed this decline to seasonal factors, emphasizing that it does not indicate a weakening demand environment. Despite the reduction, TCS continues to focus on fresher hiring, with plans to onboard over 40,000 freshers for FY25 and increase campus hiring in the next fiscal year. The company is also investing in upskilling its workforce, logging over 40 million learning hours year-to-date.

The LTM attrition rate increased slightly to 13%, within TCS’s comfortable range of 11-13%. Over 25,000 promotions were awarded in Q3, reflecting TCS’s focus on career growth. Management noted that there is no direct correlation between quarterly headcount changes and business growth, with significant hiring in Q1 and Q2 balancing Q3's seasonal optimization. TCS’s diverse workforce comprises 152 nationalities and 35.3% women, demonstrating its commitment to inclusivity and strategic talent management.

What’s Ahead?

With this earnings report, TCS has provided a much needed direction for the IT pack which is quite evident from the rally seen in the IT Index stocks.

The IT stocks didn’t show any positivity post good Accenture results, mainly due to weakness in the broader market and macro-economic woes. However, with TCS coming out with decent results, TCV momentum and positive commentary about discretionary spending making a comeback, we could expect the woes for IT sector bottoming out by Q4FY25. Of course, we also need to watch what other IT companies have to report and comment on their Q3FY25 results.