Hexaware Technologies - IPO Analysis | Should you be subscribing to this upcoming IPO?

Hexaware is making a comeback to the bourses with the largest IPO ever by an Indian IT company at Rs. 8750 crores. Should you hit that apply button? Read our analysis below:

About Company:

Hexaware Technologies is a global digital and technology services provider with AI at its core [as claimed by the company in its RHP]. It leverages technology to deliver innovative solutions that support customers in their digital transformation journey and ongoing operations.

Hexaware operates through six segments, aligned with the industries it serves: Financial Services, Healthcare and Insurance, Manufacturing and Consumer, Hi-Tech and Professional Services, Banking, and Travel and Transportation. Its offerings span five broad service categories—Design & Build, Secure & Run, Data & AI, Optimize, and Cloud Services—which form the foundation of its solutions. These services are delivered through AI-enabled digital platforms, including RapidX™ for digital transformation, Tensai® for AI-powered automation, and Amaze® for cloud adoption.

With a presence across the Americas, Europe, and the Asia-Pacific region (including India and the Middle East), Hexaware serves a diverse global customer base. Its capabilities are further strengthened by an extensive ecosystem of enterprise partnerships, which enhance customer offerings and expand market reach.

IPO Details:

Initially, the company aimed to raise $1.2 billion but later revised the offering size. The IPO, which will be entirely an offer for sale (OFS) by promoter CA Magnum Holdings, will be open for public subscription from February 12 to 14, with anchor investor bidding commencing on February 11.

The price band has been set at ₹674-708 per share. Carlyle currently holds a 95.03% stake in Hexaware. The company has significantly increased its market share, with 62% of its revenue coming from large corporations with annual revenues exceeding $5 billion. Over the past three years, the number of clients generating $20 million in revenue for Hexaware has nearly doubled, reflecting strong business growth.

Voluntary Delisting from Stock Exchange in 2020 - What Happened?

Carlyle Group, a US-based private equity firm, acquired Hexaware Technologies in October 2021 for approximately $3 billion. This acquisition came after Hexaware's previous owner, Baring Private Equity Asia, had delisted the company from Indian stock exchanges in November 2020. The delisting process was initiated in June 2020 when Baring offered to buy out public shareholders at a floor price of Rs 264.97 per share. However, after the reverse book building process, the final delisting price was set at Rs 475 per share, which was accepted by Baring. This delisting offer was successful, with Baring acquiring approximately 29% stake from public shareholders, increasing its ownership to about 91% in Hexaware. The delisting marked the first successful delisting on Indian bourses since December 2018.

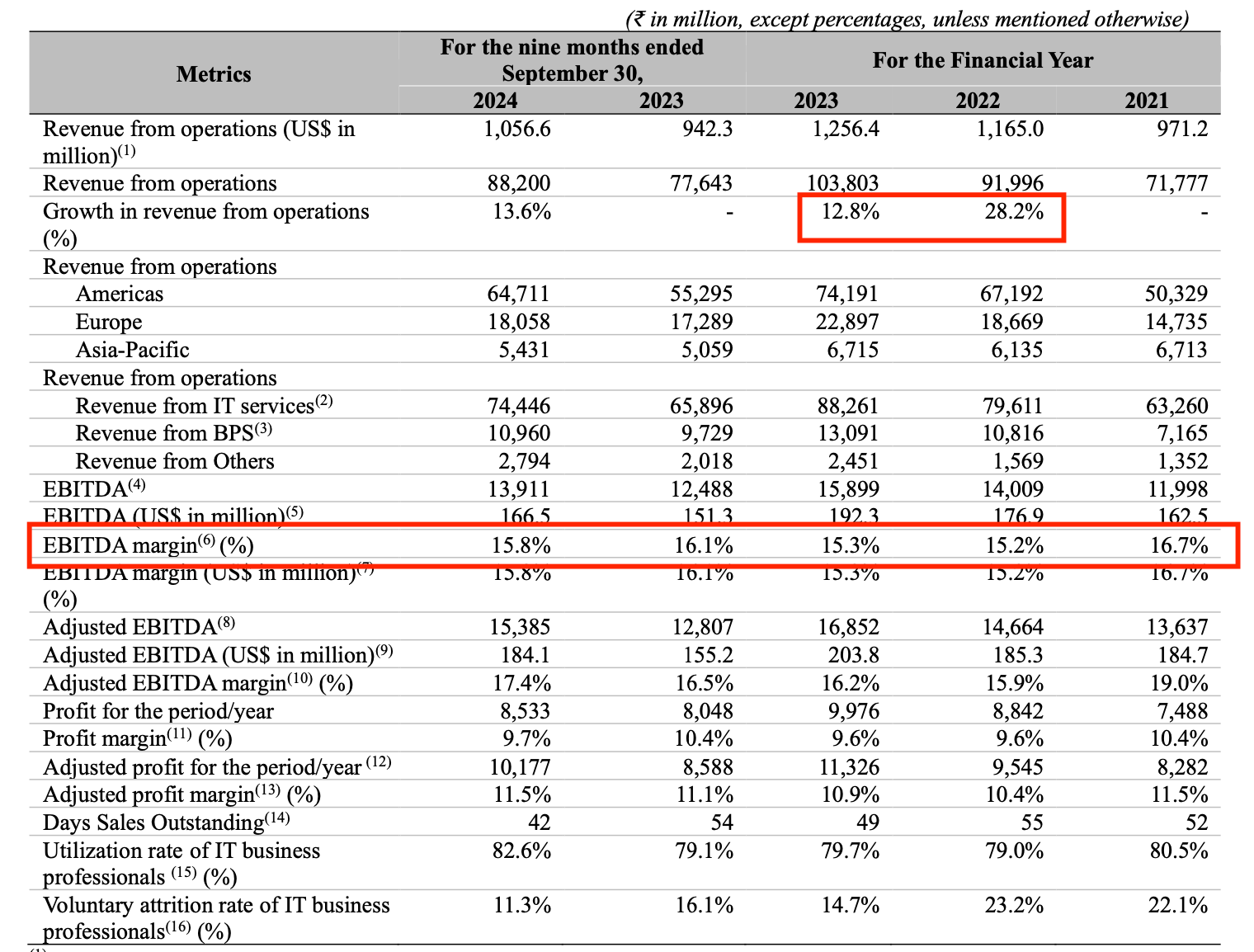

How has the company fared since it’s delisting?

The company before the delisting used to operate at a OPM of 16~17%. Since going private, the EBITDA margin has been constantly declining and hovers around 15.8%.

The company unfortunately has not been able to improve its margins despite being under a PE company known for its restructuring and operational efficiencies. The current EBITDA margin is on the lower end of what Indian Midcap IT companies operate at. The revenue growth has also been decent, but looks like the company missed the train of digital transformation boom that happened post covid.

How does Hexaware fare against its Peers:

Hexaware listed out its peers in DRHP. The peer group considered consists of Persistent Systems Limited, Coforge Limited, LTIMindtree Limited, and Mphasis Limited. The below facts and figure are taken from the RHP document. Although the KPI measurements might vary company by company, however it still provides us with a broader picture for comparison.

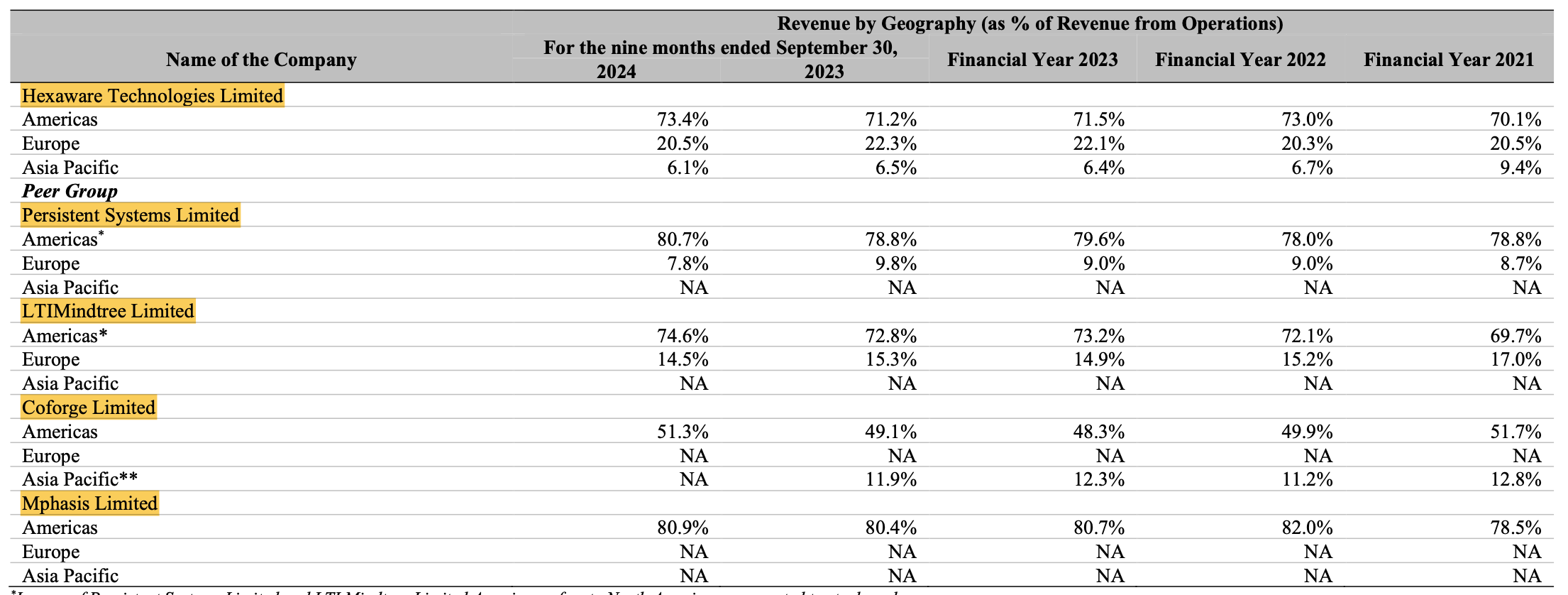

Revenue by Geographical Areas:

Indian IT companies are usually concentrated in the Americas region due to the heavy spend on IT services over there. However, over-concentration to one continent can lead to macroeconomic and geopolitical risks. Trump’s tightening of H1B visas is one such geopolitical risk associated with Indian IT companies.

Hexaware Technologies looks better positioned than Persistent, LTIMindtree and Mphasis in terms of revenue concentration in Americas. However, the best in class is Coforge here with the lowest percentage of revenue being derived from Americas region at 51.3%.

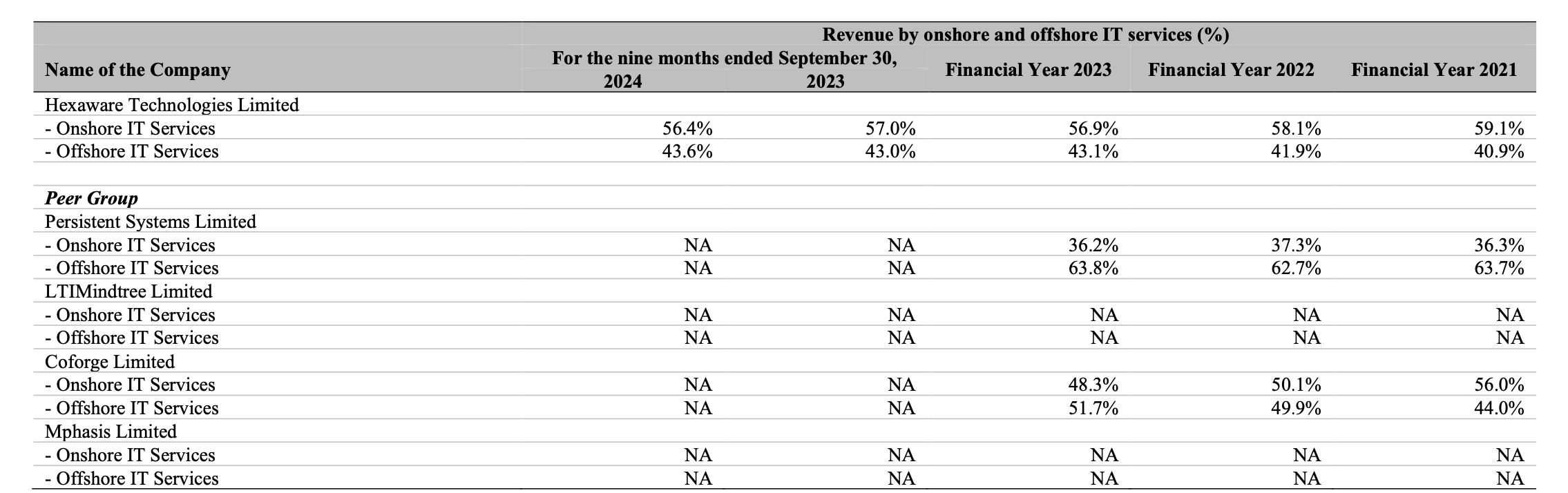

Revenue by Onshore vs. OffShore Services:

IT companies deriving greater percentage of revenue offshore are considered more profitable since the company is able to use cheaper resources in the offshore countries to keep the cost low.

When comparing to its peers, Hexaware ranks the lowest with 57% of its revenue being derived from Onshore resources. This is the primary reason why we see Hexaware not being able to keep its cost low. The best in class here is Persistent systems derving nearly 64% of its revenue from Offshore resources.

Utilization and Attrition Rate of Resources:

Both utilization and attrition rate plays an important role in analysing IT companies. These figures indicate how well the IT companies are able to utilise the resources and the rate of churn of employees.

For utilization rate, Hexaware is ranked the lowest when compared to Persistent and Coforge. However, for the attrition rate, Hexaware is the best amongst its peers indicating high satisfaction of employees. IT companies being so much Human resources dependent, high employee satisfaction becomes critical.

Where are the Acquisitions?

IT companies rely a lot on inorganic growth to expand its operations. M&A play a huge part in operations strategy for an IT firm. Hence, that’s why we see a lot of Midcap and Largecap IT companies acquiring smaller firms to expand. It’s usually much cheaper and efficient to acquire a smaller firm specializing in a technology than building the expertise for the technology in-house.

However, in the case of Hexaware, we can see that the company has only acquired two companies since 2019 i.e. Mobiquity and Softcrylic. Although, we don’t have detailed commentary from management as in why they didn’t acquire more companies, it nevertheless becomes a point of speculation and more clarity from the management would be required once they go public again.

Final Verdict:

Hexaware IPO is priced at a P/E of 41. From our analysis, we can see that the company is is performing well and growing consistently. However, from our peer analysis, we can also conclude that the companies lies behind the consistent outperformers such as Persistent and Coforge. The company seems to be better positioned than Mphasis and LTIMindtree. Both Mphasis and LTIMindtree is currently trading at a range of 35x TTM PE and Coforge and Persistent are trading at a TTM PE of ~65x. I believe, the IPO to be correctly prices at PE of 41 and it’s highly unlikely that the market would reward the company with a higher multiple post listing.

Subscribing to the IPO and buying it post-listing has been left to the discretion of the reader. We are not SEBI registered yet and this should not be construed as an investment advice. Do your own due diligence before investing.