Company Analysis #2 - Zensar Technologies

Company Analysis #2 - Zensar Technologies

A mid-tier Indian IT player with near term muted growth, but good prospect in the long term. With restructuring and strategic acquistions, the company is looking to outperform other Tier-2 IT players.

About Company:

Headquartered in Pune, India, Zensar functions as a constituent of the RPG Group, a conglomerate with a revenue of USD 4.4 billion, serving over 145 global clients. With a workforce exceeding 10,500 professionals dispersed across 30 locations worldwide, the company maintains a global presence.

Employing a velocity approach, Zensar utilizes focused speed to deliver effective outcomes, enabling its clients to navigate rapidly changing landscapes. Through the integration of speed and direction, the organization aids enterprises in attaining their goals and sustaining success.

Specializing in crafting and delivering engaging, cutting-edge digital experiences, Zensar seamlessly incorporates the latest technologies to meet client needs. Adopting a comprehensive lifecycle approach, the company combines creative, consulting, and technological expertise to develop innovative products and services, supporting its clients' digital transformation objectives.

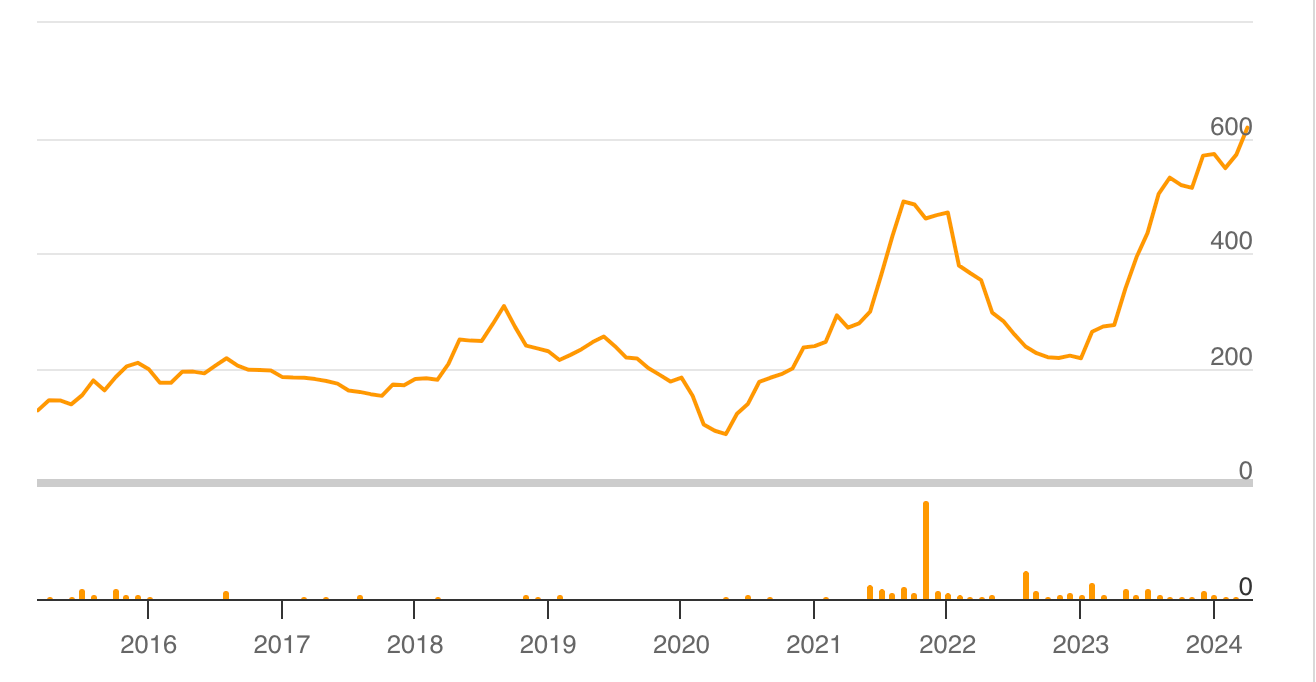

Price Chart:

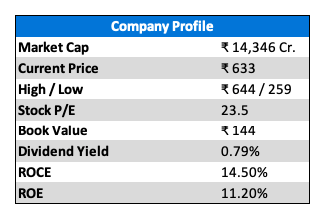

Company Market Profile:

Customer Profile:

Zensar is recognized as a technology solutions provider serving a wide array of clients globally, numbering over 148. The company collaborates with Fortune 2000 firms in sectors such as banking, financial services, insurance, hi-tech, manufacturing, retail, healthcare, and utilities. These clients often possess intricate IT infrastructures, prompting the need for specialized services to improve customer experiences, reduce operational costs, and advance digital transformation efforts.

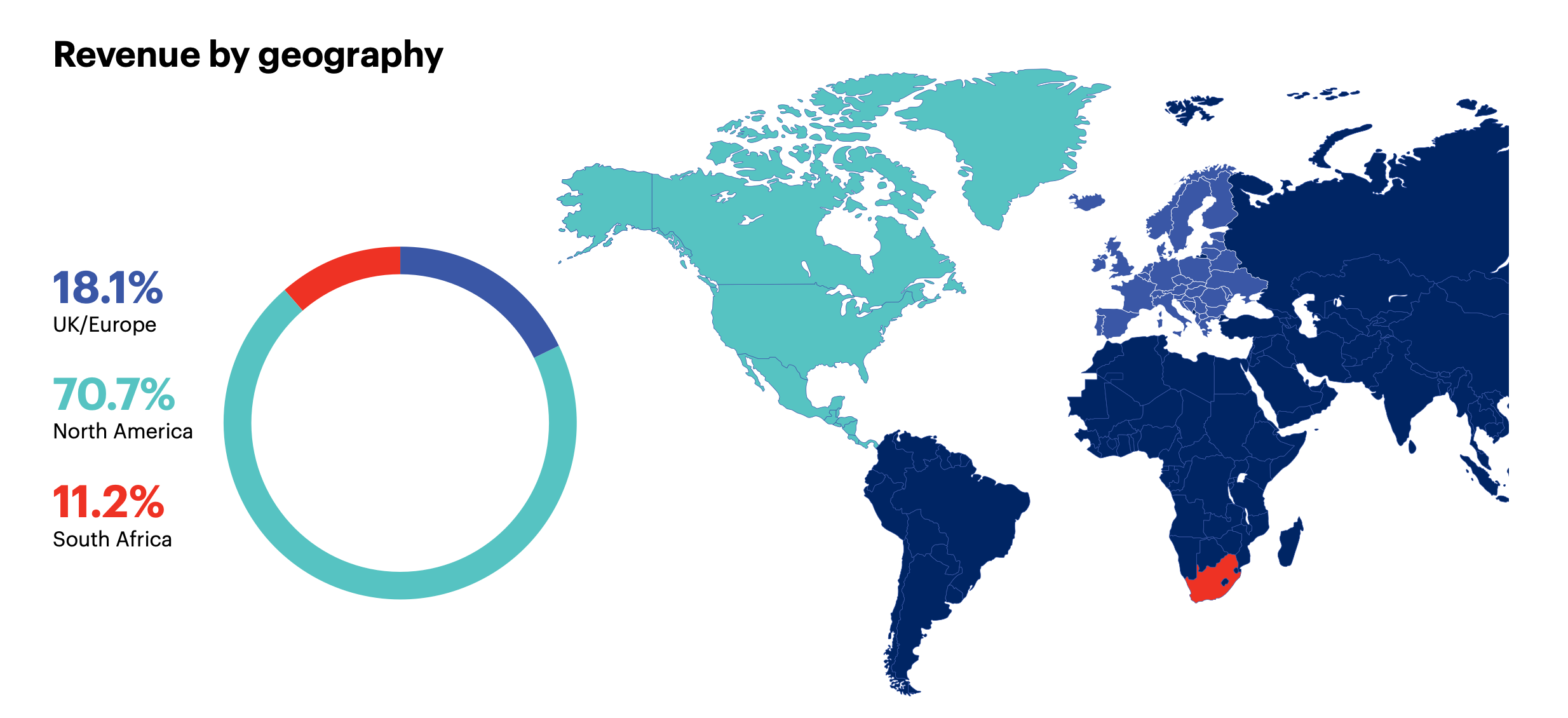

Despite macroeconomic uncertainty stemming from the Russia-Ukraine conflict, revenue in Europe has experienced a significant year-on-year growth of 20%. Similarly, the South African market has demonstrated notable growth of approximately 18.3% in constant currency. However, the company's U.S. operations have faced a slowdown, impacting overall performance.

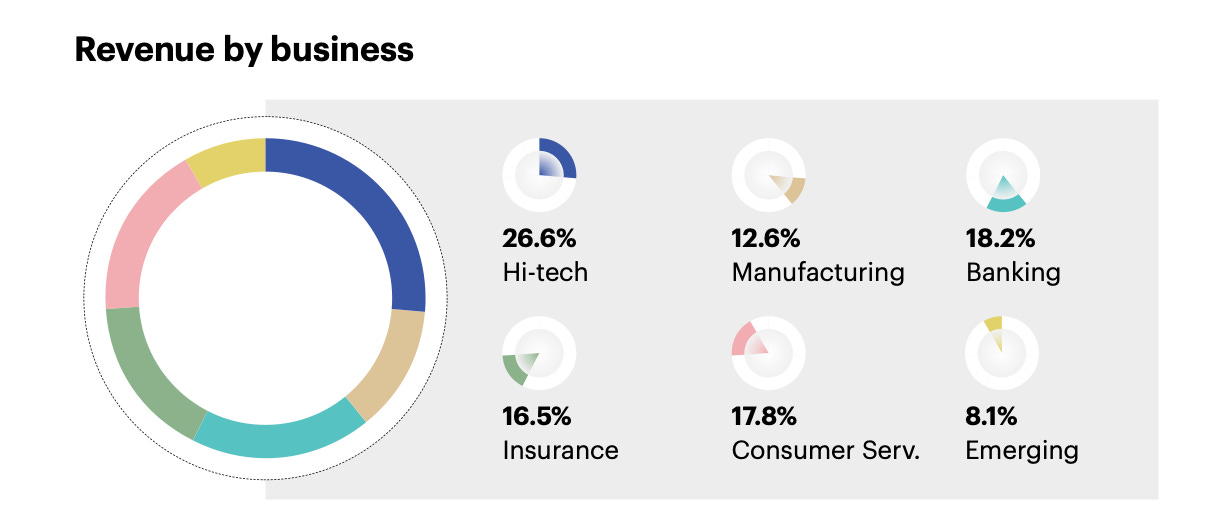

Zensar primarily operates in three industries: Hi-Tech & Manufacturing (HTM), BFSI, and Consumer Services. While revenue growth in BFSI has been commendable, registering a growth of 22.3% driven by new wins and existing customers, the HTM and Consumer Services verticals have experienced relatively subdued growth.

Zensar’s North American operations has majorly focused on the HTM vertical which has shown considerable slowdown in the region. Hence, the company is now focusing on expanding BFSI and Consumer Services sector in the region.

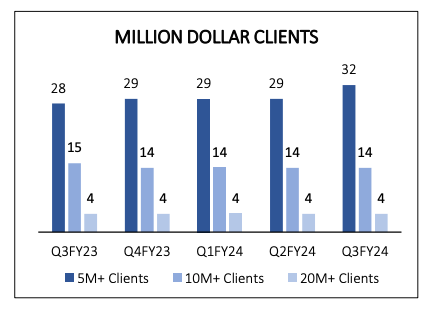

From the above chart, we see that the firm has onboarded 4 new $5M clients in past four quarters. Clients with $20M order book value has remained constant whereas the clients with $10M order book value has decreased from 15 to 14. Not shown in the chart, but smaller clients with $1M in order book has also declined from 87 to 84 over past 4 quarters. Overall, the number of active clients has reduced from 148 four quarters ago to 147 in the recent most quarter.

Product Offerings:

Experience Services (9.4% of the Revenue): Experience services is all about optimizing customer experiences of their clients. This services include optimizing client’s current website or building new one for them and also consulting on brand and marketing strategies.

Advanced Engineering Services (17.6% of the Revenue): Advanced Engineering Services include AI Engineering Buddy, Cloud Transformation and Digital Engineering strategies. Zensar is leveraging OpenAI’s Ecosystem to upgrade legacy code of the clients. The directive is to empower engineering teams to expedite their software development journey, ensuring the confident delivery of high-quality solutions while addressing their code intellectual property concerns, resulting in efficiency gains of at least 30 percent as claimed by Zensar.

Data Engineering and Analytics (8.6% of the Revenue): Zensar leverages data analytics offerings by software giants such as Microsoft Azure, Power BI, Tableau to empower clients to better understand their data.

Application Services (45.8% of the Revenue): Application services makes up the biggest offering by Zensar. They have partnered up with Salesforce, SAP, and Oracle to implement/upgrade their softwares and also provide consulting services on how clients can better cater these services to their business model.

Foundation Services (18.5% of Revenues): Zensar’s Foundation Services is all about “Manage(ing), operate, and optimize IT infrastructure for the best business outcomes”

At Zensar, substantial investments are directed towards emerging technologies like AI/ML, blockchain, quantum computing, and Web 3.0/metaverse. These efforts are overseen by the innovation division, Zenlabs. The company's strategic investments have positioned it as a leader in these emerging fields, bolstering its capability to pursue novel business prospects.

Corporate Governance:

Zensar is overseen by Mr. Harsh Goenka, who also holds the position of Chairman at RPG Enterprises, of which Zensar is a part.

In December 2022, the company appointed Mr. Manish Tandon as its CEO and Managing Director. With over 27 years of experience, Mr. Tandon brings a proven track record of driving industry-leading revenue, profit, and growth. Prior to joining Zensar, he served as the CEO of CSS Corp, a US-based technology services company, where he played a key role in its turnaround and consistent growth. Mr. Tandon's extensive experience includes a 20-year tenure at Infosys Limited, where he led a global business spanning healthcare, financial, insurance, life sciences, and technology sectors, with revenues exceeding $2 billion. According to his LinkedIn bio, Manish operates from New Jersey, United States.

Key Company Risks:

Indian ITes companies commonly face various risks and some of them that is also true for Zensar are:

Heavy reliance on the Americas Region: Like most of the Indian IT companies, Zensar also derives most of it revenues from the United States. The U.S. is currently facing macroeconomic headwinds which has led the Federal Reserve to signal that they won’t be cutting the Interest Rates as expected this year. This leads to business uncertainty and underinvestment in discretionary IT spending that Indian IT companies are heavily reliant on.

One good thing for Zensar is that their business in Europe and South Africa are expanding at a commendable pace which has led the overall share of revenue from 70% to 66% y-o-y in the Americas region. According to a sectorial report by HDFC securities, despite the macro uncertainties in Europe, discretionary IT spending has remained strong and is also expected to pick up in the upcoming quarters.

Revenue concentration amongst top customers: The company has about 147 active customers, but has been deriving nearly 58% of their revenue from just 20 customers and 30% of the revenue coming from just 5 customers. Although from the chart below, we see that the revenue concentration mix has been improving in the recent quarters, still the risk remains significant. Loss of one client in the top 20 list can mean a minimum loss of revenue anywhere between 3-6%.

Source: Company’s Presentation

Management Discussion & Analysis:

In the latest earnings call, the management has highlighted the mitigation measures they are taking to improve client penetration and revenues:

The company is especially focusing on their new services offering of Experience Services and Advanced Engineering Services. Recent quarters have shown these two offering verticals picking up which will provide more earning stability to the company.

They are also trying to adopt to the latest trends in the tech industry and are upgrading their offerings with Generative AI.

The company is also heavily focusing on M&A where they are looking at a potential acquisition target every week. The company has a good reserve of cash that can be utilized in the M&A activities acquiring strategic targets. They are specifically looking for targets that can help them serve clients in the Healthcare sector better.

Financial Summary:

Revenue and Profit Analysis:

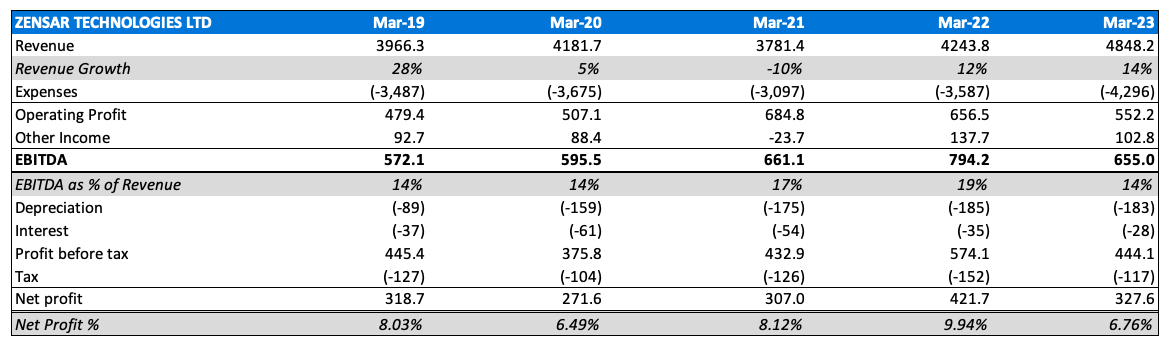

Zensar’s 10-year Revenue CAGR stands at 9% and 5 -year CAGR is at 5%. The company has seen some really muted growth in its revenue in an industry where other competitors have been doing really well in last 5 years owing to digital transformation boom. Most of this muted performance can be attributed to little to no growth in Hi-Tech and Manufacturing sector that makes up a significant chunk of the revenue. Zensar has been actively trying to diversify their revenue base and it will be a few quarters before we can see the result of it. Profit CAGR stands at 6% for 10-year and 5-year period.

Key Financial Ratios:

Shareholding Pattern:

Shareholding pattern has been in line with the Industry trends. Between March and December 23, we see FII buying the stock again. According to a report by Nirmal Bang, this might not be idiosyncratic to the company or even the IT Sector. 2023 saw an above average inflow into small and mid-cap indexes and hence the increase in shareholding pattern might be entirely attributable to that. Promoters stake has been fairly constant and has hovered around 49%.

Recent Deal wins:

Helping a connectivity platform provider, through Data Engineering and Analytics to integrate lot in their cloud-based product aligned to loT Security Architecture.

Integrating Advance Engineering Service solutions to tackle Security loopholes for one of the USA's smart cities by reducing cost and advancing their existing technology to give better business uptime.

Transforming legacy payment application for corporate customer through digitalization for South Africa's major banking services firm.

Digital Foundational Service to migrate and upgrade Global E-business instance on AWS cloud for one of the largest vacation ownership companies

Delivered end to end Product engineering on microservice architecture for one of the largest payment corporations